Concerned about the printed circuit board industry: a comparative analysis of the status quo of Chinese and foreign development

Guide: With the development of science and technology, printed circuit boards are widely used in high-tech fields such as military, communications, medical, electric power, automotive, industrial control, smart phones, and wearables. Therefore, the production technology level of PCB board has gradually become an important indicator to measure the level of science and technology in a country. However, compared with the development status and trends of the printed circuit board industry in foreign countries, what stage is China's printed circuit board industry, what problems exist, and how to solve it. This is the question that this article tries to answer.

Second, Asia has become the global PCB leader, and China is at the center of the Asian market.

Third, the global PCB product structure is increasingly optimized, and the future development trend is clear.

After that, the demand for major application fields will be strong in the future, and the PCB industry will have strong pull.

Second, the regional distribution pattern of the domestic PCB industry has been formed.

As an important electronic component, a printed circuit board is a support for electronic components. Because of its important role in the field of electronic components, it has become "electronic aircraft carrier" by many people. With the development of science and technology, printed circuit boards are widely used in high-tech fields such as military, communications, medical, electric power, automotive, industrial control, smart phones, and wearables. Therefore, the production technology level of PCB board has gradually become an important indicator to measure the level of science and technology in a country. However, compared with the development status and trends of the printed circuit board industry in foreign countries, what stage is China's printed circuit board industry, what problems exist, and how to solve it. This is the question that this article tries to answer.

First, the concept and characteristics of printed circuit boards

A printed circuit board, that is, a printed circuit board or a printed circuit board, is cut into a certain size by using an insulating board as a base material, and has at least one conductive pattern attached thereto, and is provided with a hole (such as a component hole and a fastening). Holes, metallized holes, etc., are used to replace the chassis of electronic components of conventional devices, and to achieve interconnection between electronic components. Because it is made by electronic printing, it is called a "printing" circuit board. The function of the PCB board is to provide a base that integrates the components of the hierarchical structure with other necessary electronic circuit components to form a module or a finished product with a specific function, so the PCB board plays an integrated connection function in the entire electronic product. The role of the formation.

The current circuit board is mainly composed of lines and drawings, dielectric layers, holes, solder mask inks, silk screens and surface treatment. The circuit is used as a tool for conducting conduction between the originals. In the design, a large copper surface is additionally designed as a grounding and power supply layer, and the wiring and the drawing are often made at the same time. The dielectric layer is used to maintain the insulation between the lines and the layers, commonly known as substrates. The via hole allows the two or more layers to be electrically connected to each other, and the larger via hole is used as a component insert. In addition, the non-conductive via is usually used as a surface mount and is used for fixing screws during assembly. The solder resist ink is mainly used to protect the circuit on the printed circuit board, prevent the circuit from being oxidized, and cause open circuit or short circuit due to careless wiping. According to different processes, the solder resist ink can be divided into green oil, red oil and blue oil. Silk screen is a non-essential component. The main function is to mark the name and position frame of each part on the circuit board to facilitate post-assembly maintenance and identification. After that, since the copper surface is easily oxidized in a general environment, it is impossible to apply tin (poor solderability), and therefore it is protected on the copper surface to be tinned. The protection methods include tin spray, gold, silver, tin, organic flux, etc., each having advantages and disadvantages, collectively referred to as surface treatment.

Printed circuit boards have grown rapidly and are used in a wide range of applications, primarily due to the many advantages of their collection. First, due to the repeatability (reproducibility) and consistency of the PCB board graphics, wiring and assembly errors are greatly reduced, saving equipment maintenance, commissioning and inspection time. Designed with standardization, high wiring density, small size and light weight, it has the characteristics of replaceable line, convenience, precision and miniaturization, especially the bending resistance and precision of FPC flexible board. PCB boards are irreplaceably applied to high precision instruments. Its mechanized and automated production increases labor productivity and reduces the cost of electronic equipment. It is precisely because of the above characteristics and advantages of the PCB board that the application field of the PCB board is expanded and characterized. The production technology level of PCB boards has gradually become an important indicator to measure the development of science and technology in a country.

Second, the development status of the printed circuit board industry

1. Development status of China's printed circuit board industry

At present, the development of the global printed circuit board industry has embarked on a relatively stable development period, and has formed seven major production centers including Hong Kong, Japan, Taiwan, South Korea, the United States, Germany and Southeast Asia, including Asia. It accounts for 79.7% of the global GDP. China has become an important global printed circuit board production base due to its advantages in industrial distribution and manufacturing costs. In 2013, China's circuit board production value has accounted for more than 44.2% of the global total output value, but the market share of individual Chinese enterprises. Smaller, the dominant ability in the market is not strong.

In the past two decades, the development of China's PCB industry has been very rapid through the introduction of foreign advanced technology and equipment. In 2002, China's PCB output value surpassed Taiwan and became the world's third largest PCB producer. In 2003, China's PCB output value and import and export volume exceeded US$6 billion, making it the second largest PCB producer in the world. In 2006, China surpassed Japan. It has become a global PCB manufacturing base and has become a global PCB production site for five consecutive years. In 2010, China's PCB production value increased rapidly to 18.5 billion US dollars, and the global share rose to 35.3%. In 2011, the global PCB output value reached 55.409 billion US dollars, China's PCB output value growth remained stable, and the global share rose to 39.8%. In 2012, the global PCB industry was affected by the global economic weakness, and the growth rate declined. China's PCB production value still occupied a high global market share. As the economy recovers, it will continue to grow from 2013 to 2016.

2. Development status of the global printed circuit board industry

Since the mid-1950s, PCB technology has been widely adopted. At present, PCB has become the "mother of electronic products", and its application has almost penetrated into various terminal fields of the electronics industry, including computers, communications, consumer electronics, industrial control, medical instruments, defense military, aerospace and many other fields. In the future, with the exhibition of the new generation of information technology industry, emerging electronic products such as smart phones, automotive electronics, LED, IPTV, digital TV and so on will continue to emerge, and the use and market of PCB products will continue to expand.

In recent years, the global PCB industry has generally grown steadily. In 2009, affected by the global financial crisis, PCB output value declined. In 2010, with the gradual improvement of the global macro economy, the PCB industry began to recover. The annual output value reached US$52.468 billion, a significant increase of 27.33% compared with 2009.

China Industrial Information Network released "2016-2022 China PCB market depth survey and investment prospect analysis report" pointed out: the global financial crisis in 2008 has caused a huge impact on the PCB industry, China's PCB industry has also been affected, the national PCB The total output value of the industry dropped from US$15.037 billion in 2008 to US$14.252 billion in 2009, down 5.2% year-on-year. In 2010, China's PCB industry experienced a full recovery. The total output value of the national PCB industry reached US$19.071 billion, up 40.1% year-on-year. From 2011 to 2012, as the global electronics industry and PCB industry entered an adjustment period, the growth of China's PCB industry also slowed down. The total output value of the national PCB industry was US$22.029 billion and US$22.034 billion, respectively, with growth rates of 10.30% and 0.02% respectively. . In 2013-2014, the total output value of the national PCB industry recovered, with growth rates of 11.62% and 6.01%, respectively. According to Prismark (a professional consulting firm in the US electronics industry, hereinafter referred to as “Prismarkâ€), the annual compound growth rate of China's PCB industry output value is 5.1% in 2014-2019. According to Prismark's forecast, the overall scale of the global PCB industry will reach 72.07 billion US dollars in 2016, and the global PCB production growth rate will be 5.38% from 2011 to 2016.

3. Development status of the US printed circuit board industry

The US PCB industry structure is also biased towards hard-board production. The proportion of hard-board accounts for more than 70%. The proportion of high-rise board production is higher than that of Japan and Taiwan. 12 to 20 layers account for 21% of the total PCB products. 22-layer board or more accounts for the whole camp. 13% of the total, the above 12-layer board products accounted for more than 30% of the proportion, 4 to 10-layer board accounted for 17%. In the field of flexible board and soft and hard board, the main manufacturer in the United States is Multi-FinelineElectronix, which is mainly based on soft board assembly. The products are widely used, among which mobile phones are the main applications, including customers such as Apple, RIM and Motorola.

In terms of product application, the US PCB industry employs PCBs for mobile phones as the main application products, accounting for 26%. Multi-Fineline is the representative of mobile phone soft boards, and Multek produces HDI boards for mobile phones. US PCB industry's secondary products account for 19% and 18% of telecom equipment-related applications and computer-related products. TTMTechnologies, Inc. is the leading provider of communications infrastructure equipment applications in the US, and its PCB products are used in aerospace and defense applications. There is also a high proportion of adoption; in addition, the United States is also one of the major suppliers of PCBs for servers, and the world's first PCB makers are the US, and the US manufacturers account for 40% of the global market. Above; in addition, the US PCB industry has a considerable investment in the automotive, medical and military PCB boards. According to the “2016-2022 China PCB Board Industry Market Analysis and Investment Prospect Research Report†released by the Industry Information Network, the proportion of US PCB companies in the past 100 has been shrinking in recent years, but the total output value has remained stable (about the global total). The amount of 4.6%) and the average output value increased slightly, mainly due to the merger between enterprises; it is expected to remain unchanged or slightly decline in the next few years.

4. Development status of the Japanese printed circuit board industry

According to Prismark statistics, the proportion of Japan's printed circuit board industry's output value to the global market has declined in recent years. In 2014, the regional market output value was 6.62 billion US dollars, accounting for 11.5% of the global market.

Japanese PCB manufacturers focus on the production of high-end and high-priced PCB products, mainly based on soft boards and soft and hard boards, which together account for about 47% of the overall production PCB, mainly used in mobile phones and HDD, IC carrier board accounted for 30 %, the above two together accounted for 77% of the total, hard board products only accounted for 21%, and is a high-tech and popular HDI board.

In terms of product applications, the Japanese PCB industry is mostly used in the field of IC packaging, accounting for 30%, which is also the reason why Japanese companies produce high proportion of IC carriers. In this field, the world's major Ibiden revenue is high, the products are FCBGA and FCCSP applications, and the Japanese company ShinkoElectric is also the leader in this application, mainly based on FlipChip, P-BGA and P-CSP substrates. Japan's PCB board is used in the mobile phone field, accounting for 25% of the overall production; Nippon's ranking, more than 30% of its product portfolio, are mobile-related applications, including LCD soft-board for mobile phones;

Ibiden's applications on mobile phones are mainly HDI and AnylayerHDI. The Japanese PCB manufacturers in the mobile phone customer base, mainly Apple and Nokia, etc., so the continued growth of the smart phone market, the Japanese PCB industry will also help. Automotive-related applications account for 13% of Japan's PCB production value. Although the proportion is not as good as other applications, Japanese PCB industry's product supply for automotive PCBs has led the world, such as CMK and Meiko.

Third, the development trend of the printed circuit board industry

1. The development trend of the global printed circuit board industry

After decades of development, the PCB industry has become a global industry. In recent years, the output value of the global PCB industry accounts for more than 1/4 of the total output value of the electronic component industry. It is a major industry in the electronic component segmentation industry and has a unique position. In order to actively respond to the development needs of downstream products, PCBs are gradually developing in the direction of high density, high integration, fine lines, small aperture, large capacity, light and thin, and the technical content and complexity are continuously improved.

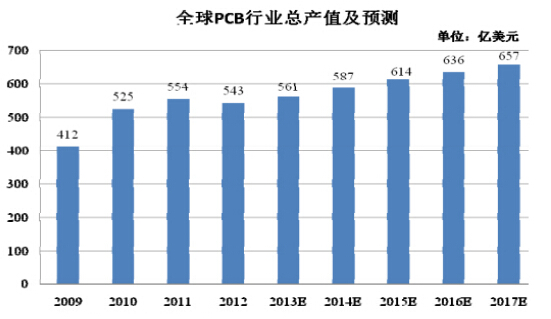

First, the global PCB industry will maintain steady growth.

According to China Industry Insights Network statistics and forecasts, the global PCB output value in 2010 was 52.568 billion US dollars, an increase of 27.3% compared with 2009; in 2011, global PCB output value reached 55.409 billion US dollars, an increase of 5.6% compared with 2010; 2012 global PCB output value reached US$54.31 billion, a 2.0% decrease from 2011; from 2012 to 2017, the global PCB will maintain a steady growth rate of 3.9%, and the overall size in 2017 is expected to reach US$65.654 billion.

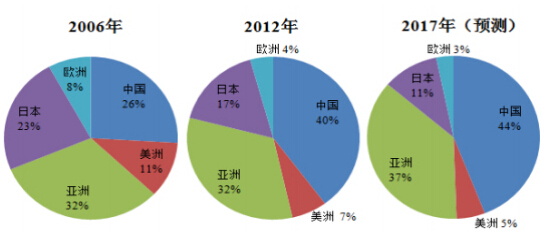

Second, Asia has become the global PCB leader, and China is at the center of the Asian market.

Before 2000, 70% of global PCB production value was distributed in Europe, America (mainly North America) and Japan. Since the beginning of the 21st century, the focus of the PCB industry has continued to shift to the Asian region, forming a new industrial structure. The PCB output value in Asia is close to 90% of the global total, which is the dominant PCB in the world, especially in China and Southeast Asia. According to China Industrial Insight Network, since 2006, China has surpassed Japan to become a global PCB manufacturing base with large output value and rapid growth, and has become the main growth driver for the development of the global PCB industry. In 2012, China's PCB output value reached 21.636 billion US dollars, accounting for 39.84% of the global PCB output value. From 2008 to 2012, the annual compound growth rate of China's PCB production value reached 9.52%, higher than the global growth level. According to Prismark, China's PCB production value will reach 28.972 billion US dollars in 2017, accounting for 44.13% of the global total output value.

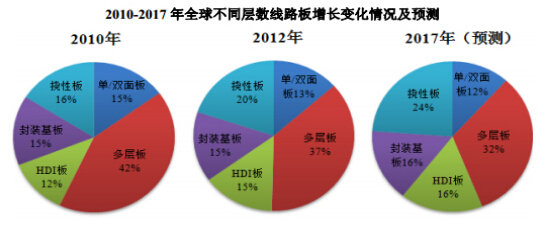

Third, the global PCB product structure is increasingly optimized, and the future development trend is clear.

As downstream electronic products pursue light, thin, short and small development trends, PCBs continue to develop in the direction of high precision, high integration, and thinness. In 2011, the global single/double panel total output value increased by 0.4% compared with 2010; the multi-layer board output value increased by 1.1%, and its total volume still dominates the PCB board; HDI board increased by 17.4%, which is in the PCB board. The type of growth in output value; the growth rate of output values ​​of package substrates and flexible boards were 6.6% and 12.4%, respectively. In 2012, global single/double panel output value decreased by 8.7% compared with 2011; multi-layer board output value decreased by 9.1%, still in the main position; HDI board output value increased by 5.8%, continued to maintain a good growth trend; package substrate output value decreased by 4.7%; The output value of flexible boards increased by 17.2%. According to Prismark, the global PCB industry will continue to develop steadily in the future. HDI boards and multi-layer boards will maintain a good momentum of development; from 2012 to 2017, the compound growth rate of HDI boards will reach 6.5%, becoming the main growth point of the PCB industry; The compound growth rate of multi-layer boards will reach 1.2%.

After that, the demand for major application fields will be strong in the future, and the PCB industry will have strong pull.

The good development momentum of the electronic information industry is the basis for the growth of the PCB industry. The continued high prosperity of the PCB downstream sector will drive the rapid development of the PCB industry. With the development of modern technology, the downstream field of PCB is currently experiencing favorable opportunities for technology upgrades and product replacement. The replacement cycle of the top three computer, communication and consumer electronics products is steadily shortening. The new consumption hotspots have made the PCB industry face a broader market space and scale of demand. According to statistics and forecasts of China Industrial Insight Network, the global electronic system product output value in 2010 was 1.756 billion US dollars, reaching US$1.99 billion in 2012, and will reach US$2.369 billion in 2017, with an average annual compound growth rate of 4.41%.

2. China's printed circuit board industry development trend

First, China's PCB industry maintains rapid growth.

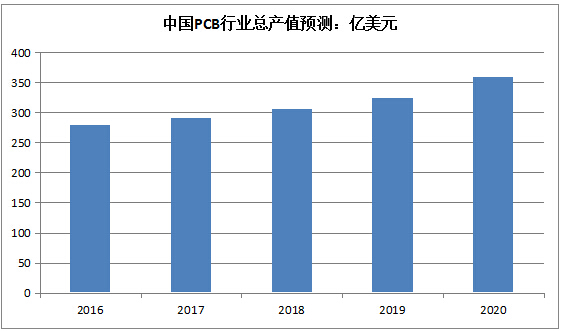

Looking into the future, the global PCB industry will continue to develop in the new round of growth cycle. The growth of demand in the terminal application market will continue to drive the continuous development of the upstream industry. More and more innovative application terminal electronic products will emerge from the outside world. The PCB industry offers more market growth points. As far as China is concerned, with the steady recovery and continuous transformation of China's economy, the development of China's PCB industry will usher in more opportunities in the next few years: First, the continuous transfer of industries and the establishment of world-renowned PCB companies in China. The cluster advantage of China's PCB industry will be further highlighted, and it will also encourage more local enterprises to grow and develop faster, and push the technological strength and management level to a new level through fierce market competition and learning effects. Secondly, “Ten During the Second Five-Year Plan period, the development of seven strategic emerging industries will provide more development opportunities and policy support for the development of Chinese PCB enterprises; after that, consumption is expected to occupy a more important position in driving the economic growth troika, domestic consumption. The rapid development of the market will further promote the expansion of the application market and indirectly drive the development of the upstream PCB industry. According to Prismark, China's PCB industry will continue to grow rapidly in the next few years, and its global market position will continue to increase. From 2012 to 2017, China's PCB output value will grow at a compound annual growth rate of 6.0%. By 2017, the total output value will reach US$28.872 billion, accounting for 44.13% of the global PCB output.

Second, the regional distribution pattern of the domestic PCB industry has been formed.

According to the statistics of CPCA, there were about 1,500 domestic PCB industry enterprises in 2013, mainly distributed in the Pearl River Delta, Yangtze River Delta and Bohai Rim. PCB production in the Yangtze River Delta and Pearl River Delta accounts for about 90% of China's total output value; PCB production capacity in the central and western regions has also expanded rapidly in recent years.

The Yangtze River Delta and Pearl River Delta regions are regions where domestic electronic technology products are more developed, and are also the birthplace of IT and PCB. They enjoy unique advantages in terms of geography, talents and economic environment, and are currently in the stage of industrial upgrading. The low-end products in the PCB gradually shifted to other parts of the interior, while products and high value-added products continued to be concentrated in the Yangtze River Delta and Pearl River Delta regions. In the future, the domestic PCB industry is likely to form a research and development base for PCB manufacturing, equipment and materials in the Pearl River Delta and Yangtze River Delta; a two-hour economic industry with the world's top 500 electronics companies including Chongqing, Sichuan, Hubei, Anhui, etc. along the Yangtze River. Belt; the Bohai Bay Economic Circle led by Dalian in the north; and the industrial pattern of the processing area in the northwest of Guangdong after the opening of the Hong Kong-Zhuhai-Macao Bridge.

After that, the main structure of domestic PCB products tends to be diversified and

According to the statistics of CPCA, since 2000, various types of PCBs in China have been obviously developed. The development speed of multi-layer boards, HDI boards and flexible boards is higher than the average development speed of the industry, and the development speed of single-panel and double-panel is relatively stable.

From the perspective of domestic PCB product development trends, the increase in output is slightly lower than the increase in sales, mainly due to the gradual development of product structure to multiple layers and high precision. China's multi-layer board and HDI board are in the growth stage of the industry, the scale is expanding, and the process is becoming more mature. Multi-layer boards are still the mainstream of market development; while HDI boards are driven by the demand for upgrading of downstream electronic information products, they are in a period of rapid development.

Fourth, the development of China's circuit board industry and its countermeasures

From the above analysis, the Chinese PCB industry has experienced rapid development from the mid-to-late 1980s to the present, after more than 20 years of development, and has experienced three stages of development, including state-owned economy, Sino-foreign joint ventures and foreign-owned enterprises. A remarkable achievement. China's PCB industry has a dominant position in the world.

With the rapid development of IT industry and electronic machine manufacturing in China, the PCB companies all over the world have also made large-scale investments in China. The scale, output and output value of China's PCB manufacturing industry have been among the best in the world. . In particular, the price of the medium and low-end PCB has a strong competitive ability. As the whole machine develops toward high performance and miniaturization, its difficult PCB production is also increasing. In the near future, China's PCB will occupy an important position in the world.

However, we have to admit that there is a gap between the Chinese PCB industry and the level of R&D and production technology between developed countries. Specifically, the challenges facing the Chinese PCB industry are as follows:

First, R&D and production technologies are relatively backward. With the rapid development of electronic technology and the increasing demand for “short, small, light and thin†electronic products, the demand for PCB product technology must be rapidly improved. The demand for high-layer, thin-line fine-hole and fast-transfer PCB is constantly increasing. increase. For each manufacturer, it means that there must be a large capital investment, and it is necessary to greatly improve the capabilities of the technical personnel and the overall technical strength of the enterprise. In the face of these challenges, in addition to actively carrying out talent pools and strengthening personnel training and training, the factory hopes that the government can provide certain policy support and support from the perspective of cultivating and building its own enterprises. At the same time, the government should invest funds. Independently establish research institutions or cooperate with representative enterprises to carry out research on PCB frontier technology and provide new technology services and support for domestic enterprises.

Second, the industry is chaotic and vicious competition is serious. At present, the industry has serious vicious competition in the production and operation of general products, such as uneven development, irrational investment and rapid expansion. The profit level is declining and the profitability is poor, which will seriously affect the health of the industry. development of. Based on this, it is recommended that each manufacturer proceed from its own actual situation, actively promote its self-technical ability or make full use of its own advantages, and create its own core competitiveness with distinctive operations, avoiding low-level vicious competition.

Third, the strictening of environmental protection requirements by the international community is a major challenge facing China's PCB industry. Most of China's PCB companies are small and medium-sized enterprises. They have not been able to keep up with the needs of users in the mastery and improvement of lead-free technology. Faced with a wide variety of lead-free technologies and large differences in user demand, each manufacturer needs to invest in multiple aspects, resulting in increased investment costs and increased technical adaptability and technical management. This problem can only enable industry players to eliminate this impact better and more effectively through a more detailed division of labor and cooperation.

After that, the rise in raw material prices and the fall in the price of downstream electronics seriously undermined the profits of the PCB industry in the middle. In the face of severe living space, enterprises should increase investment in technology and R&D, master the core technologies of PCB production, and change the simple profit model.

(Original title: Comparative analysis of the status quo and development of the printed circuit board industry)

Ps Cutlery,Ps Material,Soup Spoon,Ps Cutlery For Sale

Taizhou Polybest Household Product Co.,Ltd , https://www.polycutlery.com